How the expansion of FIEs has institutionalised CSR practices in China

How the expansion of FIEs has institutionalised CSR practices in China

Foreign-invested enterprises (FIEs) have helped contribute to China’s rapid economic growth with an essential component being its impact on corporate social responsibility (CSR) institutionalisation. Due to marked differences in China’s CSR environment, FIEs require additional insight if they want to continue and successfully navigate the domestic business environment. Ailin Zhou, intellectual property (IP) assistant at Taylor Wessing, analyses and advises on the complexities of CSR in China.

China’s rapid economic growth continues to have an ever- increasing influence in the global marketplace. This article tries, from the perspective of corporate social responsibility (CSR), to demonstrate how FIE expansion has impacted CSR institutionalisation in China. Due to a marked difference in CSR definitional support between developed and developing countries, along with differences in political and organisational structures in China, FIEs require additional insight into the particularities of the Chinese CSR framework and the subsequent stakeholder concerns.

The expansion of FIEs and their role in institutionalising Chinese CSR practices

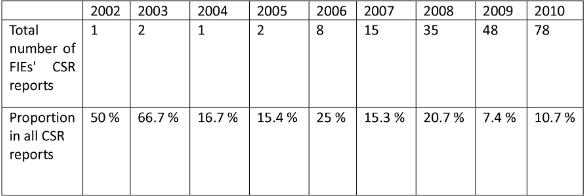

In spite of soaring economic growth, CSR remained for many years an underdeveloped concept in China. This contrasted with other, more ‘developed’, countries such as Sweden, Germany, the United Kingdom and the United States. After China’s entry into the World Trade Organization (WTO) in 2001 and among an increase of FIEs being formed in China, massive changes took place in the Chinese institutional environment. According to the Research on Social Responsibility Report of Foreign-Invested Enterprises in China (2002–2010), only one FIE was recorded as operating in China in 2002, however that number has since swelled to 78 starting in 2010. This correlates with the proportion of FIEs, state-owned enterprises (SOEs) and other (private, township or restructuring) enterprises that reported their activities utilising a CSR framework, the number of reports of which proceeded to decrease from 50 per cent in 2002 to 10.7 per cent in 2010.

Given that CSR can be used as a method of ensuring accountability and since enterprises try to attract inward investment and incentives through the use of CSR reports, the aforementioned changes indicate that FIEs attach significant importance to CSR reports and when facing the expansion of FIEs, Chinese enterprises have begun to pay attention to these reports in order to remain competitive for outside investment and government support.

The theory of CSR is believed to have emerged, and developed, for the Western world and thus may have little to contribute to Asian economies. Due to this preconception, little is now known about CSR practices in non-Western countries.[1] In spite of that, research indicates that although CSR and corporate social performance (CSP) are used for accountability and marketing purposes, top-CSR performers are trumpeted as leaders to be followed, which further institutionalises CSR practices in their respective fields.[2] These FIEs tend to have a better and more mature understanding of CSR, something that is routinely acknowledged by Chinese stakeholders. A comparative study revealed that CSP of FIEs regarding employee benefits, tax liability and environmental liability is strong, yet improvements are still needed in the customer and supplier relationship.[3]

Various associations and magazines organise events and competitions for FIEs in order to improve their CSP and to better localise their CSR strategies. For example, the China Association of Enterprises with Foreign Investment (CAIFI) together with the China WTO Tribune hold an annual competition that showcases excellent CSR practices by FIEs. These exemplary CSR practices, carried out by outstanding FIEs, are subsequently examined by researchers and then imitated by competitors. The expansion of FIEs in China has influenced the domestic institutionalisation of CSR practices, although this process has been constantly challenged by domestic Chinese enterprises.

The Chinese CSR framework and organisational field

Undoubtedly, globalisation has affected how CSR is perceived by businesses and FIEs are, to some extent, powerful actors in the Chinese CSR field. Yet, in order to improve the influence and visibility of CSR programmes, FIEs need to better understand the unique Chinese CSR framework and subsequent organisational field.

Highlighting these differences, rén (仁) and lǐ (礼) in Confucianism form the foundation of the Chinese concept of CSR.[4] The word rén refers to “benevolence, philanthropy, and humaneness”, while lǐ is usually interpreted as “social rules and norms that dictate legitimate behaviour”.[5] Research suggests the strong Confucian ethics of rén and lǐ are often seen as “a substitute for the concept of CSR by a number of Chinese business leaders”.[6]

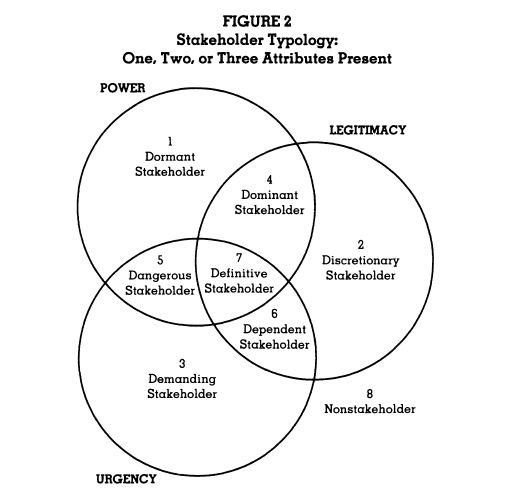

In addition to traditional Confucian values, collectivist cultural orientation also plays a prominent role in Chinese business development.[7] Juelin Yin and Yuli Zhang have developed a framework for understanding CSR in China, as illustrated in Figure 2 below. They offer two explanations for China’s adoption of this current CSR framework. The first is that, in the ‘Chinese institutional context’, “stakeholder interest and legal compliance” are not treated as crucial CSR components because of China’s transitioning financial and legal systems.[8] The second explanation pertains to the “dominant influence of ethical leadership in China”.[9] In contrast to China, where many market-based transactions are governed by ‘managerial ethics’, many western-economic transactions are governed by both formal and informal institutions.[10] The Chinese Government-led market economy has instead been characterised by unclear property rights, an ineffective legal framework and having a lax monitoring force.[11]

Research has found that the legal infrastructure underpinning existing tax law and other forms of state regulation have impacted corporate behaviour in socially responsible ways.[12] Having different levels of regulation can properly incentivise corporations to behave in a particular manner in order to achieve certain political goals.[13] Since 2006, the Chinese Government at the national, provincial and local level, has been promoting CSR as a way to rebuild social legitimacy.[14] The difficulty that comes with adopting CSR as a wider societal model is that, “businesses are not really responsible to society in general, but only to their stakeholders”.[15]

Adopting a stakeholder classification model, the dominant members of society that have an actual stake in promoting CSR are local governments. However, local governments in China are much less powerful than their national counterparts and therefore they must accept the central government’s CSR rules and guidelines despite not having the greatest interest in ensuring they are enforced.[16] Despite these shortcomings, localities try and further institutionalise CSR practices by offering incentives, holding CSR conferences and forums, and by setting up special committees to observe local businesses in their operations.[17]

Figure 3. classification of stakeholders (Mitchell, R.K., Agle, B.R., & Wood, D.J., 1997, Toward a Theory of Stakeholder Identification)

Figure 3. classification of stakeholders (Mitchell, R.K., Agle, B.R., & Wood, D.J., 1997, Toward a Theory of Stakeholder Identification)Past research has examined the methods used by local governments in China to facilitate corporations’ CSP. In both provinces and municipalities that include, the city of Shanghai, Jiangsu Province, Zhejiang Province, Guangdong Province, Hebei Province, Shanxi Province, Shaanxi Province and Hainan Province, programmatic documents have been put forward to help conceptualise CSR. In addition, provincial standard vary remarkably.[18] Research also points out the gaps and differences in guiding ideology and understanding of CSR. These differences often lead local governments to adopt different methodologies for improving corporate social behaviour.[19]

Hao Qin’s (one of the main drafters of the three national standards) comparative study provides some insights into the different methods that local governments primarily use when crafting CSR. One method that is used is to withdraw from any support-related activities completely, since it depends on the organisation’s philanthropic nature to voluntarily shoulder the burden of CSR. This method is often utilised in underdeveloped areas that are disproportionately impoverished. The second method is to enact new regulations, since organisations and the local government can cooperate strategically in order to achieve both their stated economic and CSR-related goals. This method is often employed in relatively less-developed or developing areas like Hebei and Shanxi Province.[20] The government, in this case, functions as an interlocutor that helps to balance profit-seeking motives and corporate social behaviours. The government seeks to achieve this by encouraging, promoting, and enacting ‘soft laws’ that establish mechanisms to enforce accountability. The last method is to simply enact regulatory standards and strictly apply them. These standards need to be supervised underneath a continuous system of accountability. Cases in point are Hangzhou in Zhejiang Province, Shenzhen in Guangdong Province and the Pudong district in Shanghai.[21] These areas tend to be more developed with large-scale exchanges between FIEs and international academics.

Conclusion

From the above-mentioned, it is obvious that FIE expansion has a positive impact on the Chinese CSR field. However, FIEs are facing increasingly fierce competition, as Chinese enterprises are now aware of the importance of CSR. Chinese enterprises may be better attuned to Chinese stakeholder expectations and local policies, so in this light FIEs need to provide advanced access to needed, relevant information. More importantly, FIEs need a better understanding of the Chinese CSR framework along with local rules and regulations in order to continue and improve CSR programmes.

[1] Lindgreen, A., Swaen, V., & Campbell, T. T., 2009, Corporate Social Responsibility Practices in Developing and Transitional Countries: Botswana and Malawi, Journal of Business Ethics, vol. 90, no. 3, pp. 429-440.

[2] Yin, J., Rothlin, S., Li, X., & Caccamo, M., 2013, Stakeholder Perspectives on Corporate Social Responsibility (CSR) of Multinational Companies in China, Journal of International Business Ethics, vol. 6, no. 1-2, pp. 57-71.

[3] Liu, Y., & Zou, Z., 2012, Comparative Study: The Social Responsibility of Foreign-funded Corporate in China, Scientific Research, International Conference on Engineering and Business Management, pp. 226-229.

[4] Liu, X., China’s Traditional Culture, Huanzhong University of Science and Technology Publisher, Wuhan, 1998; and Lü, X. H., 1997, Business Ethics in China, Journal of Business Ethics, vol. 16, no. 14, pp. 1509-1518.

[5] Yin, J., & Zhang, Y., 2012, Institutional Dynamics and Corporate Social Responsibility (CSR) in an Emerging Country Context: Evidence from China, Journal of Business Ethics, vol. 111, no. 2, pp. 301-316.

[6] Ibid.; Liu X., 1998, China’s Traditional Culture; and Lü, X. H., 1997, Business Ethics in China.

[7] Axinn, C. N., Blair, M. E., Heorhiadi, A., & Thach, S. V., 2004, Comparing Ethical Ideologies Across Cultures, Journal of Business Ethics, vol. 54, no. 2, pp. 103-119.

[8] Yin, J., & Zhang, Y., 2012, Institutional Dynamics and Corporate Social Responsibility (CSR), p. 312.

[9] Ibid.

[10] Ibid.

[11] Yin, J., Rothlin, S., Li, X., and Caccamo, M., 2013, Stakeholder Perspectives on Corporate Social Responsibility (CSR) of Multinational Companies in China, Journal of International Business Ethics, vol. 6, no. 1-2, pp. 57-71; Tan, J., 2009, International Structure and Firm Social Performance in Transitional Economies: Evidence of Multinational Corporations in China, Journal of Business Ethics, vol. 86, no. 2, pp. 171-189.

[12] Campbell, J. L., 2007, Why Would Corporations Behave in Socially Responsible Ways? An Institutional Theory of Corporate Social Responsibility, Academy of Management Review, vol. 32, no. 3, pp. 946-967.

[13] Ibid.; Galaskiewicz, J., 1991, Making Corporate Actors Accountable: Institution-building in Minneapolis St.Paul. in W. W. Powell & P. J. DiMaggio (Eds.), The New Institutionalism in Organizational Analysis, pp. 293-310. Chicago: University of Chicago Press.

[14] Moon, J., & Shen, X., 2010, CSR in China Research: Salience, Focus and Nature, Journal of Business Ethics, vol. 94., no. 4, pp. 613-629.

[15] Avetisyan, E., & Ferrary, M., 2013, Dynamics of Stakeholders’ Implications in the Institutionalization of the CSR Field in France and in the United States, Journal of Business Ethics, vol. 115, no. 1, pp. 115-133.

[16] Mitchell, R. K., Agle, B. R., & Wood, D. J., 1997, Toward a Theory of Stakeholder Identification and Salience: Defining the Principle of Who and What Really Counts, Academy of Management Review, vol. 22, no. 4, pp. 853-886.

[17] Wang, X. and Yang, L., 2013, Path Choice on Corporate Social Responsibility Public Policy: The Comparative Study between Six Developed Nations and China, Proceedings of the 2013 International Conference on Public Administration, vol. 1, no. 1, pp. 583-590.

[18] Hao, Q., 2013, A Comparative of Local Governments’ CSR Policies, China Market, no. 11, pp. 71-76. (in Chinese).

[19] Gao, J., 2015, A Study on the Policies and Methods Local Governments Adopt in Promoting CSR, Organisation Reform and Management, vol. 7, pp. 188-190. (in Chinese); Yu, Z. H., 2010, Chinese Local Government Engages in Promoting CSR, China WTO Tribune, no. 88, pp. 83-84.

[20] Hao, Q., 2013, A Comparative of Local Governments’.

[21] Ibid;Yu, Z. B., 2008, Chinese Local Government Push Forward CSR: Treating CSR as an Effective Way to Build Well-off Society, China WTO Tribune, no. 60, pp. 56-58.

Taylor Wessing is a leading full-service law firm with over 1,200 lawyers in 33 offices around the world. Their China Group members are based in Shanghai, Beijing, Hong Kong, Munich, Frankfurt, Düsseldorf, Hamburg, Vienna, Paris, London and Singapore. Besides all areas of business law relevant to business transactions in China, they are also well known for their advice to Chinese companies investing overseas. For more information, please visit their website.

Recent Comments