How to Seize the Opportunity of Industrial Upgrade

How to Seize the Opportunity of Industrial Upgrade

In recent years, China has grown to become the world’s largest shipbuilder. However, there is a considerable gap to close for China to become a strong shipbuilding country in terms of value and technology. This article by L.E.K. Consulting looks at the challenges for Chinese shipyards to gain a competitive edge in the global market and outlines the key questions that companies and investors that are contemplating or already involved in the Chinese shipbuilding market should consider.

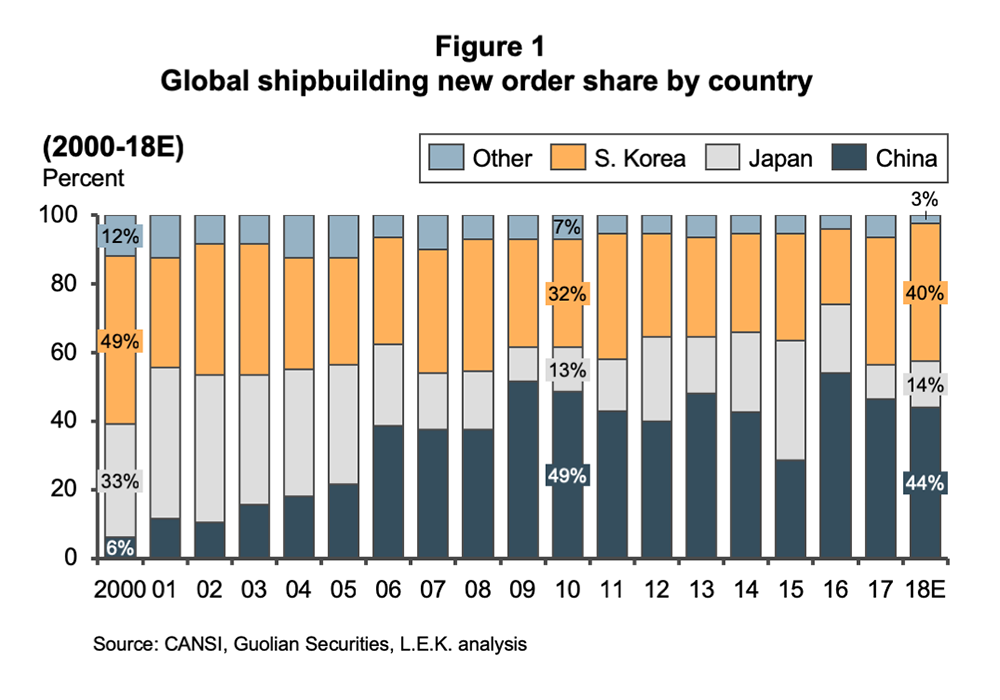

In recent years, China has surpassed Japan and South Korea in all three major shipbuilding indicators —orderbook, new orders and completions—becoming the world’s largest shipbuilder. Four out of the top 10 global shipyards are Chinese companies, and those four Chinese yards account for 45 per cent of the top 10 yards’ orderbook in total. Although the global shipbuilding industry has faced a prolonged cyclical business downturn leading to weak demand in the past few years, China still maintains a relatively stable share of the international market due to its cost and price advantages. China’s shipbuilding industry delivery volume will remain stable over the next few years.

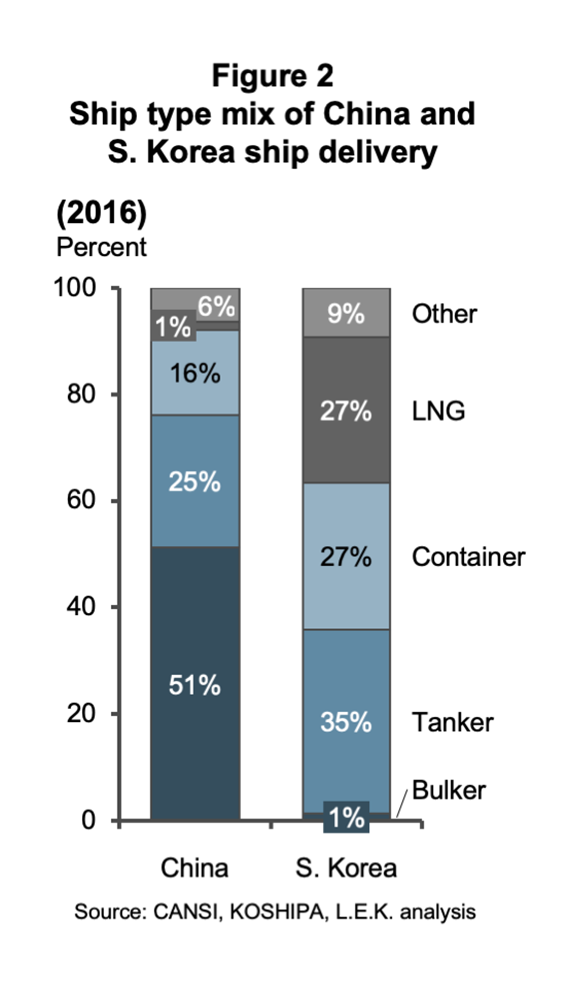

However, there is a considerable gap to close for China to become a strong shipbuilding country in terms of value and technology. China’s existing production capacity is still dominated by low value-added and low-tech ship types. The bulkers account for about 50 per cent of the total delivery, and the three mainstream cargo vessels—bulkers, tankers and containerships—together account for more than 90 per cent. Coupled with sluggish demand caused by the cyclical downturn in the downstream shipping industry over the past few years, overcapacity is serious in low-end vessel production, especially in a large number of small and midsize private enterprises. On the other hand, high value-added ship types such as LNG, LPG, special engineering vessels, Ro-pax and luxury cruise vessels have shown insufficient capacity.

There are serious challenges for Chinese shipyards trying to gain a competitive edge in the global market. After decades of relying on low-cost and capacity advantages, China’s shipbuilding industry now needs to upgrade to a more refined way of development. In recent years, the Chinese Government has issued a series of guidance and action plans for the shipbuilding industry: Made in China 2025 clarifies the overarching strategic objective to become a nation strong in high-end shipbuilding and offshore engineering equipment manufacturing. Shipbuilding Industry Deepening Structural Adjustment, Accelerating Transformation and Upgrading Action Plan (2016-2020) put forward by the China Ministry of Industry and Information Technology (MIIT) proposes a series of plans such as eliminating low-end production capacity, increasing R&D investment, improving industry concentration level and efficiency, and achieving breakthrough in construction of large luxury cruise vessels. The Ship Equipment Industry Capacity Improvement Action Plan lays out the objectives of improving product spectrum and increasing the localisation rate of core ship equipment and components. Driven by market demand and industrial policies, there are three major market trends we have observed emerging in China’s shipbuilding and ship equipment industries.

There are serious challenges for Chinese shipyards trying to gain a competitive edge in the global market. After decades of relying on low-cost and capacity advantages, China’s shipbuilding industry now needs to upgrade to a more refined way of development. In recent years, the Chinese Government has issued a series of guidance and action plans for the shipbuilding industry: Made in China 2025 clarifies the overarching strategic objective to become a nation strong in high-end shipbuilding and offshore engineering equipment manufacturing. Shipbuilding Industry Deepening Structural Adjustment, Accelerating Transformation and Upgrading Action Plan (2016-2020) put forward by the China Ministry of Industry and Information Technology (MIIT) proposes a series of plans such as eliminating low-end production capacity, increasing R&D investment, improving industry concentration level and efficiency, and achieving breakthrough in construction of large luxury cruise vessels. The Ship Equipment Industry Capacity Improvement Action Plan lays out the objectives of improving product spectrum and increasing the localisation rate of core ship equipment and components. Driven by market demand and industrial policies, there are three major market trends we have observed emerging in China’s shipbuilding and ship equipment industries.

Continuous industry transformation and upgrade

In recent years, Chinese shipyards have taken actions to increase their R&D investment, strengthen management systems, and continuously optimise their product mix. These actions have led to breakthroughs

in a series of high-end vessel types, including the 2,500-passenger luxury Ro-pax, 7,800-parking space Ro-

Ro, 84,000 cubic-metre ultra-large LNG vessels, 38,800-ton duplex stainless steel chemical tankers, 20,000 TEU mega-containerships and 350,000-ton FPSOs. China’s first high-profile luxury cruise project is also steadily progressing. In 2017, the China State Shipbuilding Corporation (CSSC) signed a memorandum of agreement with Carnival Corp. and Fincantieri S.p.A. to collaborate on the construction of China’s first luxury cruise ship. The cruise ship owner—the operating company formed by the CSSC, Carnival and the China Investment Group—will order the first series of 2+4 133,500 GT Vista-class luxury cruise liners from the cruise-building company jointly established by the CSSC and Fincantieri. Each cruise ship would cost USD 780 million and be built at Shanghai Waigaoqiao Shipyard, a subsidiary of the CSSC. The project has entered the preliminary design and preparation phase, and the first ship is to be delivered in 2023.

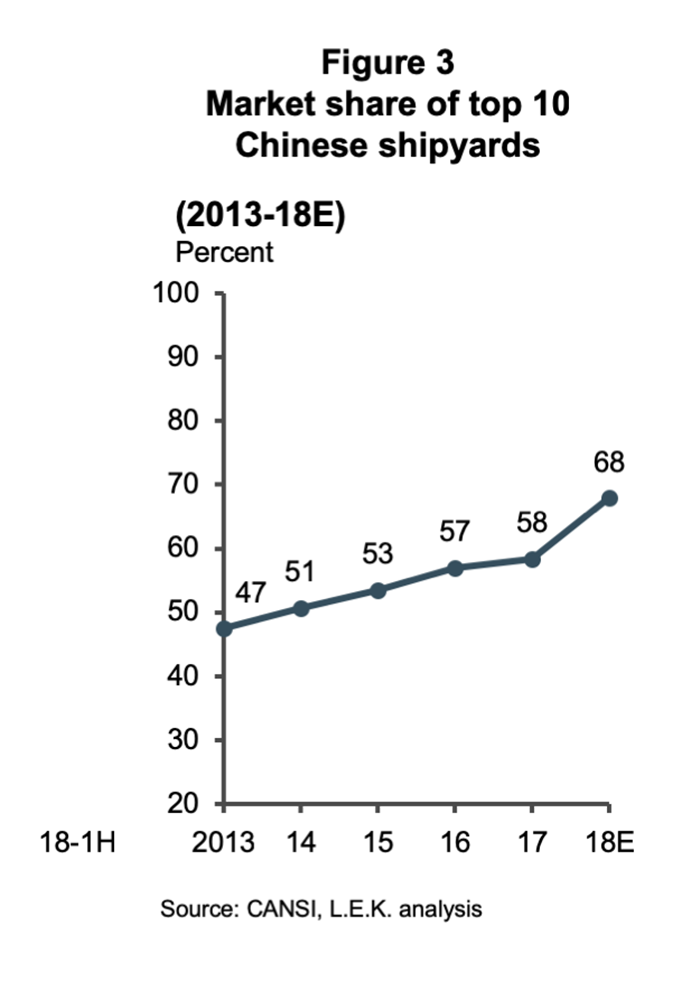

Increasing industry consolidation

Due to the joint effects of market dynamics and policy guidance, the concentration level of China’s shipbuilding industry has increased through horizontal integration and by clearing out excess low-end capacity. At the end of 2016, China Ocean Shipping Group had merged 13 large shipyards and more than 20 supporting service companies to establish COSCO Shipping Heavy Industry Co Ltd. The CSSC and the CSIC are also actively integrating and restructuring their affiliated shipyards. In the first half of 2018, the market share of the top 10 Chinese yards was 67.9 per cent, 9.6 per cent higher than 2017 and nearly 20 per

cent higher than six years ago.

Active investments in core ship equipment / components

China’s large shipbuilding companies are moving up the value chain into ship equipment/component, and carrying out vertical integration to enhance their competitiveness and profitability. The ship equipment

industry is an important part of the shipbuilding industry. Ship-specific equipment accounts for about 40 per cent to 60 per cent of total ship cost, mainly including power systems, electronic and electrical equipment, deck machinery, and cabin machinery. From a value chain perspective, due to high technical barriers and concentration levels, the upstream ship equipment industry has a much higher gross margin level than have downstream shipbuilding and assembly activities.

High-end diesel engines, propulsion systems, and communication and navigation equipment are areas with the most potential for domestic substitution. In the field of power systems, domestic low-speed, medium-speed and high-speed diesel engines have achieved breakthroughs and gained market recognition.

We believe the Chinese shipbuilding industry, which is large in scale and undergoing transformation and upgrading, has created new opportunities for ship equipment companies and investors.

• The industrial transformation and upgrades will bring more opportunities for high-end ship equipment to penetrate. With the transformation of China’s shipbuilding industry, the future upgrade of product mix to more

high-value-added ship types will bring incremental demand for high-end marine equipment.

1. Multinational ship equipment companies can secure key accounts and gain first-mover advantage by leveraging their technological advantages and relationships with global shipowners. At the same time, they

can deploy and develop distribution networks to strengthen their customer relationship management with local large shipyards. A local procurement, OEM or other viable localisation plan would reduce cost and improve price competitiveness of the products.

2. Local ship equipment companies would need to keep enhancing R&D capability to overcome the technical

barriers and catch up with global leading players to meet the demands in higher-end vessel types. The must expand market share by leveraging the advantages in customer relationships with local shipyards as well as in cost levels, cooperate with local key accounts in the global market, and last, but not least, proactively expand the overseas market by building up relationships with global shipowners.

• The cyclical downturn of the shipbuilding industry has created more M&A opportunities. High-performing companies and investors could consider acquiring and restructuring bankrupt companies or high-quality small and medium enterprises at a lower price during the downturn of the industry to benefit from the synergies in product mix, customer bases and channels, and expanding market share and industry influence. How to seize market potential and transformation opportunities is key for ship equipment manufacturers that want to realize rapid growth in the China market.

Before companies and investors make strategic decisions, they should also thoroughly consider the following key issues:

• Where will the future growth of China’s marine equipment market come from?

• What kind of organisational structure and business processes are needed to adapt to a rapidly changing market environment?

• What are the customers’ real needs and key purchasing criteria?

• What is the procurement process for marine equipment? Who is the decisionmaker and who is the influencer?

• What product portfolio can achieve maximum synergy and bundling effects?

• How can distribution networks be designed and deployed to cope with the highly fragmented market and strict market entry barriers?

• MNC companies should also consider how to compete with local players. If localisation is needed, then what is the best model? How can the proprietary know-how and brand value be protected in the localisation process?

At the same time, we also recommend that companies and investors continue to pay attention to potential risks and prepare contingency plans accordingly. Major risks may include fluctuations in the industry’s macrocycle, an increase in the regulatory entry barrier for foreign companies to enter, the escalation of global trade friction, and the risk that local competitors would gain core technological breakthroughs and thus form a competitive advantage.

L.E.K. Consulting is a management consulting firm headquartered in London (UK), with its US counterpart in Boston, MA. Founded in 1983, the company’s primary service lines consist of corporate strategy, mergers and acquisitions, and operations. It employs a generalist model across all major industries, including a large presence in defense, aviation, life sciences, healthcare, energy, entertainment, transport, retail, consumer products and financial services. The company also has a large private equity practice. L.E.K. is a global strategy consulting firm with clients and presence in the Americas, Europe and Asia-Pacific.

Recent Comments